Everyone sees the same number: trillions of dollars in US debt that need to be refinanced this year. The immediate reaction is often the same as well. This must eventually lead to a crisis.

That conclusion, however, is based on a misunderstanding of how sovereign debt actually works. The core issue is not repayment. It is pricing.

What refinancing actually means

Governments do not repay debt in the same way households do. Instead of paying it down entirely, they roll it over. When US Treasury bonds mature, new bonds are issued to replace the old ones.

This means the key question is not whether the United States can repay its debt. The more relevant question is at what cost it can refinance that debt.

That distinction is crucial. The size of the debt matters, but the price of refinancing determines how it impacts the broader economy.

Why this year matters

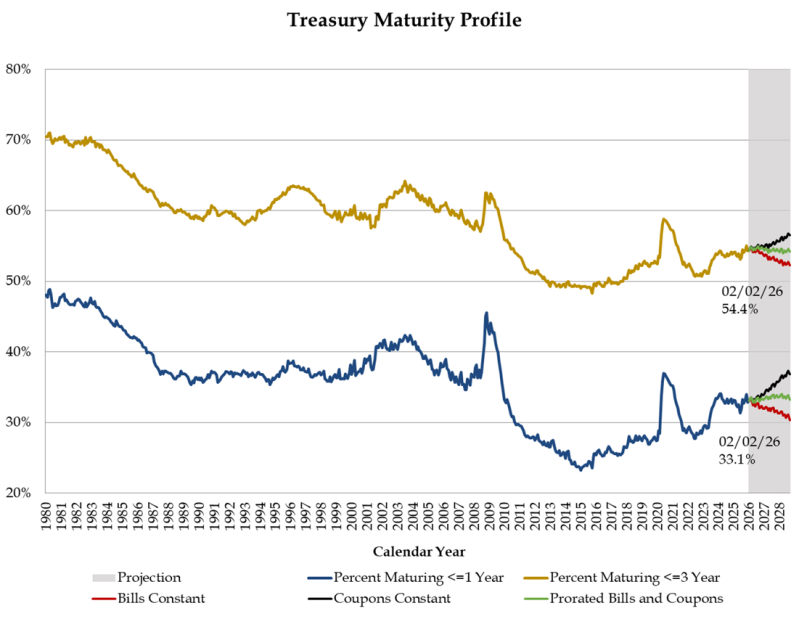

A significant portion of US government debt has a relatively short maturity. This means it needs to be refinanced frequently, causing the overall cost of debt to adjust more quickly to current interest rates.

According to data highlighted in recent US fiscal updates and cited by institutions like the Joint Economic Committee, roughly a third of marketable US debt matures within a year. That means a large share of the debt stock is continuously being repriced at current yields.

This becomes especially relevant in a higher interest rate environment. Yields today are materially above the levels seen just a few years ago. As older, lower rate debt matures and is replaced with new, higher yielding debt, the total interest burden increases.

The Treasury Borrowing Advisory Committee has also emphasized in recent quarterly refunding discussions that the scale of issuance requires sustained demand across maturities, particularly as financing needs remain elevated.

This is not a default story

Despite the scale of refinancing, this is not primarily a story about default risk. US Treasuries remain one of the most important assets in the global financial system, serving as collateral, liquidity instruments and reserve assets.

As noted repeatedly by the International Monetary Fund and echoed in coverage by the Financial Times, demand for US government debt tends to adjust with yields. When yields rise, they attract buyers.

Higher yields are therefore not necessarily a sign of failure. They are part of the adjustment mechanism that keeps the system functioning.

But it does come with a cost

While the system remains functional, the consequences of higher refinancing costs are real. As yields increase, the US government faces rising interest expenses.

The Congressional Budget Office has projected that net interest costs are becoming one of the fastest growing components of federal spending, reflecting the shift to higher rates.

The effects extend beyond government finances. Higher yields influence borrowing costs across the economy. Mortgage rates tend to remain elevated, credit conditions tighten, and financing becomes more expensive for both households and businesses.

As the Financial Times has noted in recent analysis, this dynamic effectively tightens financial conditions even without additional rate hikes from the Federal Reserve.

Where the real risk sits

The more relevant risk is not an inability to refinance, but increased sensitivity within the system. As refinancing costs rise, the system becomes more dependent on stable demand and orderly market conditions.

Recent reporting by Reuters has pointed to growing sensitivity in US Treasury markets, particularly during periods of geopolitical stress and volatility in energy markets. These episodes can reduce liquidity and make price adjustments more abrupt.

If disruptions occur, such as shifts in foreign demand or temporary dislocations in funding markets, the adjustment process can become more volatile. This does not necessarily lead to failure, but it can lead to sharper repricing.

That is typically when markets begin to react more strongly.

The bigger picture

This is not about a single failed auction or a sudden breakdown. It reflects a broader structural shift. For years, low interest rates made the refinancing process largely invisible.

Now, that process is visible again.

As highlighted in both Financial Times commentary and policy discussions around US debt sustainability, the focus is increasingly shifting from debt levels alone to the cost of servicing that debt.

Debt does not disappear. It is rolled over and repriced continuously. Each time this happens, the cost feeds back into the economy through higher rates, tighter conditions and shifting capital flows.

Bottom line

The US debt situation is not best understood as an imminent default or collapse scenario. It is better seen as a transition.

A transition from a period of extremely low borrowing costs to one where money is structurally more expensive.

As multiple institutions, including the Congressional Budget Office and the International Monetary Fund, continue to emphasize, the long term challenge is not access to funding, but the rising cost of that funding.

There may be no single breaking point, but the cumulative effect is significant.

It’s not the size of the debt,

it’s how fast it gets repriced

I write about this daily on 𝕏, where context moves faster than headlines.

Add comment

Comments