A move that doesn’t fit the usual playbook

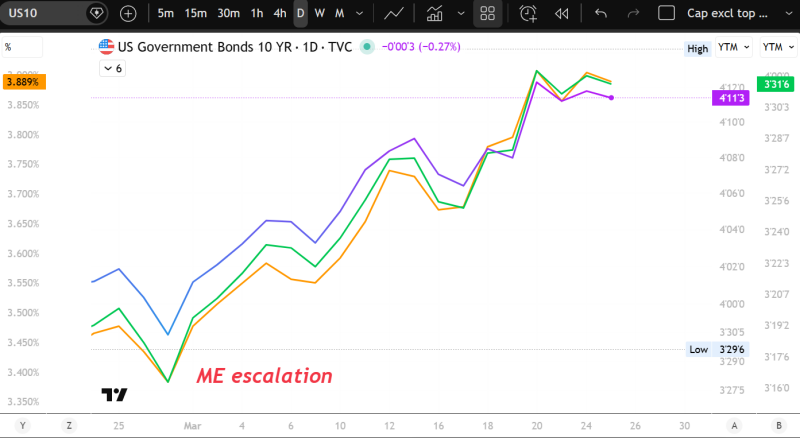

Since early March, US Treasury yields have been moving higher across the curve. Not just the 10 year, but also the 2 year and 5 year. At first glance, this coincides with the escalation in the Middle East, which makes it easy to label this as a geopolitical reaction.

But that explanation falls short.

Because when markets move on fear alone, the pattern usually looks different. In a classic risk off environment, long term yields tend to fall as capital seeks safety in duration. That is not what we are seeing now.

Instead, the entire curve is shifting higher. And that changes the interpretation completely.

What different parts of the curve actually represent

To understand why this matters, it helps to break down what each part of the curve reflects.

The 2 year yield is closely tied to expectations around central bank policy. It moves when markets adjust their view on rate cuts or hikes.

The 10 year yield reflects a broader mix. Growth expectations, inflation outlook, and what is known as the term premium, the compensation investors demand for holding longer duration assets.

The 5 year sits in between. It is often overlooked, but it plays a crucial role because it captures both policy expectations and medium term macro uncertainty.

When only one part of the curve moves, it usually tells a specific story. When all three move together, it suggests something more structural.

This is not rotation. This is repricing.

What we are seeing is not a rotation within the curve. It is not short term yields rising while long term yields fall, or the other way around.

It is everything moving higher at the same time.

That is a repricing.

Markets are not shifting capital from one part of the curve to another. They are demanding higher compensation across the board. And that only happens when uncertainty rises at multiple levels simultaneously.

Why geopolitics is not the full explanation

The timing of the move aligns with geopolitical escalation, but the structure suggests something deeper.

Geopolitical events can act as a trigger, but they rarely explain the full move in yields. If this were purely about fear, long term bonds would likely attract demand, pushing yields lower.

Instead, yields are rising.

This points to a different dynamic. The market is not just reacting to a single event. It is reassessing the broader environment in which that event occurs.

Three forces driving the move

There are several underlying forces that help explain why the entire curve is shifting higher.

First, inflation risk is being repriced. Even if headline inflation has cooled, the path forward is uncertain. Energy prices, supply chains, and geopolitical risks all feed into that uncertainty.

Second, expectations for rate cuts are being pushed further out. The 2 year yield reflects this clearly. Markets are becoming less confident that central banks will ease policy quickly.

Third, the term premium appears to be returning. For a long time, investors were willing to accept relatively low compensation for holding long term bonds. That is starting to change.

At the same time, supply dynamics matter. Governments are issuing large amounts of debt, and traditional buyers are not as dominant as they once were. When supply increases and demand becomes less certain, yields need to rise to clear the market.

The overlooked signal: the 5 year yield

One of the most important details in this move is the behavior of the 5 year yield.

It sits between policy and long term macro expectations. When it rises alongside both the 2 year and 10 year, it suggests that the market is not just adjusting one part of the outlook.

It is repricing the entire path forward.

This is a subtle but powerful signal. It tells us that the shift is not isolated. It is systemic.

What this means for liquidity

When yields rise across the curve, financial conditions tighten.

This is not always immediately visible in risk assets, but the transmission mechanism is real. Higher yields increase borrowing costs, reduce valuations, and shift capital allocation decisions.

Liquidity does not disappear overnight, but it becomes more expensive. And that change tends to ripple through markets over time.

Why this rarely stays contained

Bond markets often move first. They tend to reflect underlying macro conditions before those conditions become visible elsewhere.

When the entire curve shifts higher, it is a signal that the system is adjusting to a higher cost of capital.

That adjustment rarely stays isolated to bonds.

It feeds into equities, commodities, and crypto. It affects positioning, sentiment, and ultimately price.

Final thought

It is easy to focus on a single yield or a headline move. But the real signal often lies in the structure.

Right now, the structure is clear.

This is not a clean risk off move.

It is not a simple growth story either.

It is a broad repricing of uncertainty, inflation risk, and the cost of capital.

And when the whole curve moves like this, it usually means the system is being recalibrated.

Add comment

Comments